When you’re applying for a loan or credit card in India, your CIBIL score becomes your financial report card. But what exactly makes a “good” score? How rare is that perfect 900? And most importantly—how can you improve yours?

As someone who’s helped thousands understand credit scores, I’ll walk you through everything you need to know about CIBIL scores, from the basics to advanced improvement strategies.

Table of Contents

Quick Answer: What’s Considered a Good CIBIL Score?

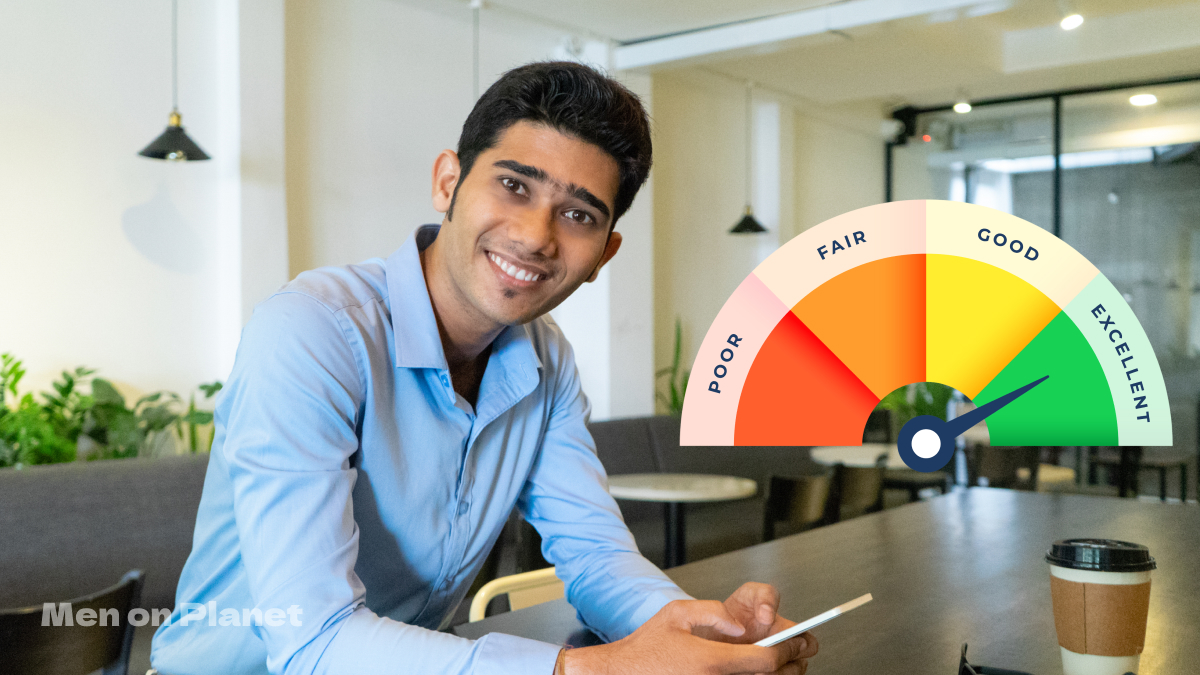

A CIBIL score of 750+ is considered excellent and will get you approved for most loans with favorable terms. Here’s the complete breakdown:

| CIBIL Score Range | Rating | What It Means |

| 300 – 549 | Poor | High risk; very low approval chances |

| 550 – 649 | Fair | Limited options, higher interest rates |

| 650 – 749 | Good | Most lenders approve with standard terms |

| 750 – 799 | Very Good | High approval rates, better interest rates |

| 800 – 900 | Excellent | Best terms, premium offers, instant approvals |

Understanding CIBIL: The Basics

What Does CIBIL Stand For?

CIBIL stands for Credit Information Bureau (India) Limited—India’s oldest and most recognized credit bureau, established in 2000.

Think of CIBIL as your financial historian. Every loan payment, credit card transaction, and even missed EMI gets recorded. Based on this history, CIBIL calculates your credit score on a scale of 300 to 900.

How Your CIBIL Score is Calculated

Your CIBIL score depends on five key factors:

- Payment History (35%) – Do you pay on time?

- Credit Utilization (30%) – How much credit do you use?

- Length of Credit History (15%) – How long have you been borrowing?

- Credit Mix (10%) – Do you have different types of credit?

New Credit Inquiries (10%) – How often do you apply for credit?

Also Read – Avoid Money Mistake in 40s

Is 750 a Bad CIBIL Score? (Spoiler: Definitely Not!)

A 750 CIBIL score is actually excellent—not bad at all! Here’s what you can expect with a 750 score:

✅ Quick loan approvals (often within 24-48 hours)

✅ Lower interest rates (sometimes 1-2% below standard rates)

✅ Higher credit limits on cards

✅ Priority customer status at banks

✅ Pre-approved offers for loans and cards

Real Example:

With a 750 score, you might get a personal loan at 10.5% interest, while someone with a 650 score pays 13.5%—that’s ₹30,000 less interest on a ₹10 lakh loan over 5 years!

The Elite Club: Who Has a 900 CIBIL Score?

A 900 CIBIL score is extremely rare—less than 1% of Indians achieve it. Based on industry data, here’s who typically reaches this pinnacle:

Typical 900 Score Holder Profile:

- Age: Usually 35+ years (longer credit history)

- Income: High and stable income sources

- Credit behavior: Never missed a payment in 7+ years

- Credit utilization: Consistently under 10%

- Credit mix: Balanced portfolio of secured and unsecured loans

- Inquiry pattern: Minimal credit applications

The Truth About 900 Scores

While 900 is impressive, you don’t need it. Banks treat 750+ and 900 almost identically in terms of loan approvals and rates.

Your Roadmap to 800+ CIBIL Score: 7 Proven Strategies

1. Master the 100% On-Time Payment Rule

Impact: Highest (35% of your score)

- Set up auto-pay for all EMIs and credit card bills

- Use mobile apps with payment reminders

- Pay at least 2-3 days before the due date

Pro Tip: Even one 30-day late payment can drop your score by 50-100 points.

2. Follow the 30% Credit Utilization Rule

Impact: Very High (30% of your score)

Keep your credit card usage below 30% of the limit. Better yet, aim for under 10%.

Example: If your credit limit is ₹1,00,000:

- ❌ Don’t spend more than ₹30,000 (30% rule)

- ✅ Try to stay under ₹10,000 (10% rule for 800+ scores)

3. Maintain Old Credit Accounts

Impact: Moderate (15% of your score)

- Keep your oldest credit card active (even if you rarely use it)

- Don’t close accounts unless there’s a compelling reason

- A 5+ year credit history significantly boosts your score

4. Optimize Your Credit Mix

Impact: Moderate (10% of your score)

Ideal mix includes:

- 1-2 credit cards

- 1 secured loan (home/car loan)

- Avoid too many personal loans or credit cards

5. Limit Hard Inquiries

Impact: Low but important (10% of your score)

- Space out credit applications by at least 6 months

- Research and apply only where you’re likely to get approved

- Check your own score monthly (soft inquiry—doesn’t hurt your score)

6. Monitor and Dispute Errors

Action: Check your CIBIL report quarterly

Common errors to watch for:

- Wrong personal information

- Accounts that aren’t yours

- Incorrect payment history

- Closed accounts showing as active

7. Build a Strong Foundation Early

For those starting their credit journey:

- Start with a secured credit card or small personal loan

- Consider becoming an authorized user on a family member’s card

- Be patient—building excellent credit takes 2-3 years minimum

CIBIL Score Improvement Timeline: What to Expect

| Action Taken | Expected Impact | Timeline |

| Pay off credit card debt | 50-100 point increase | 1-2 months |

| Start paying on time consistently | 20-50 points per month | 3-6 months |

| Reduce credit utilization to <10% | 30-80 point increase | 1-2 months |

| Dispute and correct errors | 50-150 point increase | 30-45 days |

| Build longer credit history | Gradual improvement | 6-12 months |

Red Flags That Hurt Your CIBIL Score

Avoid these common mistakes:

❌ Settling loans (shows as negative for 7 years)

❌ Becoming a guarantor for unreliable borrowers

❌ Maxing out credit cards regularly

❌ Too many loan inquiries in short periods

❌ Ignoring small dues like annual fees

❌ Not updating address/contact info with banks

Beyond the Numbers: Why Your CIBIL Score Matters

Financial Benefits:

- Save lakhs in interest over your lifetime

- Access to premium banking services

- Higher loan amounts when needed

- Better insurance premiums (some companies check credit scores)

Life Benefits:

- Reduced financial stress during emergencies

- Faster approvals when you need funds urgently

- Better negotiating power with lenders

Access to premium credit cards with rewards and benefits

Taking Action: Your Next Steps

- Check your current CIBIL score (free once a year from CIBIL.com)

- Review your credit report for errors

- Set up auto-pay for all existing EMIs and credit cards

- Calculate your credit utilization and pay down high balances

- Set a monthly reminder to monitor your score

Frequently Asked Questions

How often should I check my CIBIL score?

Monthly monitoring is ideal. It’s free when you check your own score and helps you catch issues early.

Will checking my own CIBIL score lower it?

No. When you check your own score, it’s a “soft inquiry” and has zero impact on your score.

How quickly can I improve my CIBIL score?

With consistent effort, you can see 50-100 point improvements within 3-6 months. However, reaching 800+ typically takes 12-24 months of disciplined financial behavior.

Does income affect CIBIL score?

No, your income doesn’t directly impact your CIBIL score. It’s purely based on credit behavior, not earning capacity.

Can I get a loan with a 650 CIBIL score?

Yes, but expect higher interest rates and stricter terms. Focus on improving to 750+ for better options.

What’s the difference between CIBIL and other credit bureaus?

India has four credit bureaus—CIBIL, Experian, Equifax, and CRIF High Mark. CIBIL is the most widely used, but scores can vary slightly between bureaus.

Final Thoughts

Your CIBIL score is one of the most important numbers in your financial life. While achieving 900 is impressive, remember that 750+ opens virtually all doors in the Indian financial system.

The key is consistency—pay on time, keep utilization low, and monitor regularly. Small habits today compound into significant financial advantages tomorrow.

Start with one improvement strategy this month, and your future self will thank you when you’re getting instant loan approvals at the best possible rates.